4 Tax Rules for Personal Use of Company Vehicle

The provision of business cars and allowing their personal use by employees can be one of those gestures that can set an employer apart from others in the job market. But, like other company benefits, it has documentation requirements as well as tax implications which you should account for. For starters, using a company vehicle for a purpose unrelated to the employer’s business (personal use) is a non-cash fringe benefit that is included in the employee’s taxable income.

Is All Personal Usage Taxable?

Generally, usage of company vehicles for personal trips is taxable, but here are the exceptions:

-

- The trips are so brief and occasional that they are hard to track (De Minimis Fringe Benefits).

-

- The vehicle is designed in such a way that it is improbable that someone would use it for personal errands like a school bus, ambulance, or fire truck (Qualified Non-Personal Use Vehicles).

-

- Demonstrator cars are used by a full-time auto salesperson. However, personal use only qualifies under the following conditions:

-

- It cannot be used for vacations.

-

- Only the employee is allowed to drive the vehicle.

-

- No personal belongings must be stored therein.

-

- Personal use outside of the salesperson’s normal working hours is not exempt.

-

- Demonstrator cars are used by a full-time auto salesperson. However, personal use only qualifies under the following conditions:

- The employee reimburses the company for personal use.

Rules for Reporting Personal Use of Company Vehicle as Taxable Income

The proper determination of type of usage, whether business or personal, is essential to get you and your employees’ tax liabilities right. To do this, you would need to maintain separate records of business and personal mileage. Otherwise, 100% of the value of use, including that of business, shall be treated as follows:

- It shall be included in the employee’s taxable income.

- The company won’t be able to claim a tax deduction for business use of a company car.

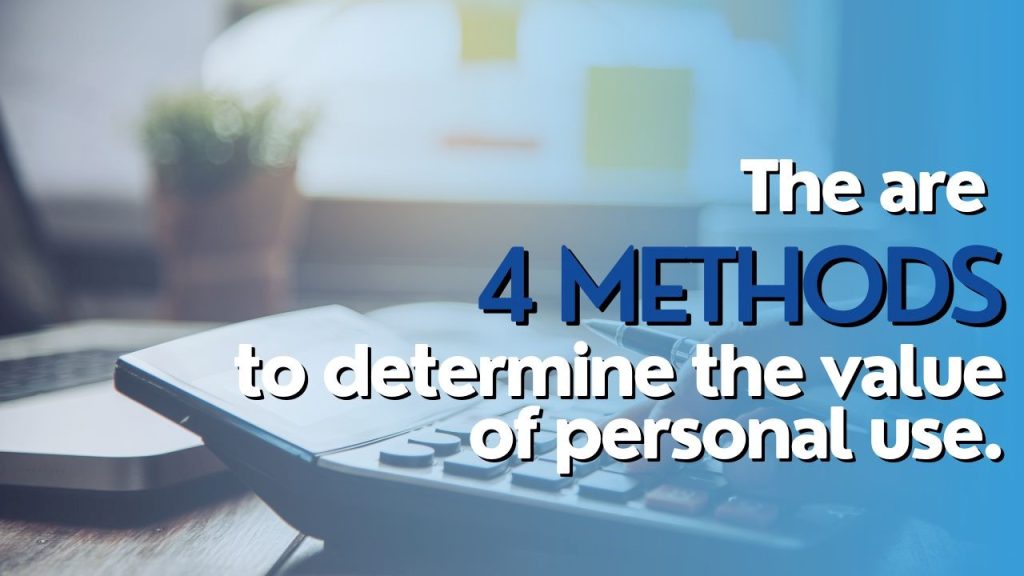

The value of personal use must be reported as income at least once a year. Such value can be determined using any of the following methods:

General Valuation Rule

Under the general valuation rule, the value of the personal is calculated based on the fair market value or the cost that the employee would have paid to a third party for the same benefit in the same geographic area and under the same or comparable terms.

Cents-Per-Mile Rule

To determine the value under this method, multiply the personal miles driven to the standard mileage rate of the Internal Revenue Service (IRS). The rate typically changes every year so it’s good to be on the lookout for any tax updates. Currently, or from July 1, 2022, through December 31, 2022, it is set at 62.5 cents per mile driven. However, either of the following conditions must be met for this method to apply:

-

- There must be a reasonable expectation that the vehicle will be used by the employee for business purposes throughout the year; or

- The vehicle must have been driven for at least 10,000 miles during the year.

Commuting Rule

You can opt for this method if:

-

- An employee uses a company car to commute to and from work.

- You have a written policy that prohibits personal use, other than de minim is personal use.

- The employee is not a control employee. In this method, you arrive at the personal use value by multiplying each one-way commute by $1.50.

Lease Value Rule

The lease value rule calculates the value by multiplying the vehicle’s annual lease value by the percentage of personal miles driven plus 5.5¢ per mile if you are providing the fuel.

The value of personal use must be included in the employee’s wages and reported at least once a year in his or her Form W-2. Employers should withhold the tax therefrom, but they may choose not to do so, as long as there is a timely notification to employees of such election and the value must be included in Boxes 1, 3, 5, and 14 of a timely provided Form W-2.

Moreover, you can opt to either calculate the income tax withholding combined with regular wages or separately at a flat 22% supplemental wage rate if the employee earns under $1 million.

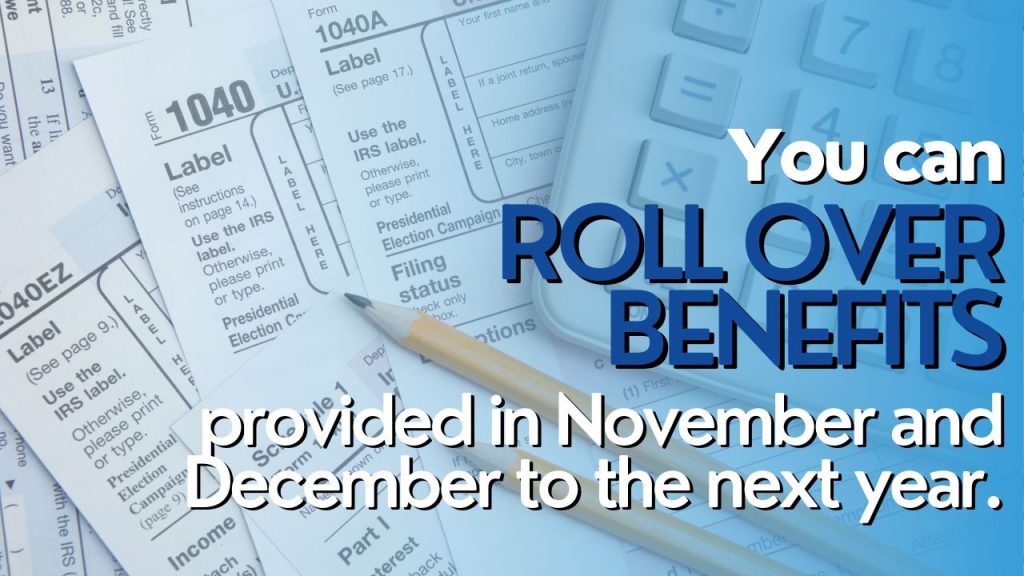

Tracking and computing the value of personal use of a business car is tedious, so you may feel like you’re strapped for a time by November and December, with tax season just right around the corner.

The good news is, you can include the benefits provided, during those two months, as paid the following year, thus, you’ll have more time to calculate the value.

Usage of a company car must be properly monitored and accounted for to avoid overpayment of taxes on the personal mileage benefit, so you don’t miss the chance to claim a deduction on your business mileage.

As with other tax rules, details such as the valuation rates may change over time, so it’s best to keep yourself informed on any updates and announcements. We’ll be happy to lend you a hand or take charge of the nitty-gritty for you. We offer full payroll tax compliance and more solutions for payroll and beyond!